Which is Better to Invest in - Stocks or Mutual Funds?

For most salaried investors in India, mutual funds are a more practical choice than investing directly in stocks. Mutual funds provide professional management, built-in diversification, and the discipline of SIP investing without requiring daily market attention. Direct stocks can deliver higher returns but demand significant time, skill, and emotional discipline. The right choice depends on how much of all three you have.

What Is the Difference Between Mutual Funds and the Stock Market?

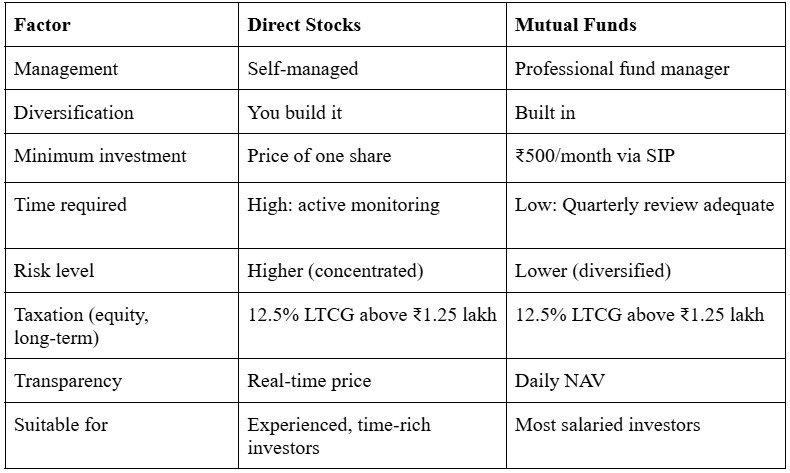

When you buy a stock, you buy a direct ownership stake in one company. Your returns depend entirely on that company's performance. When you invest in a mutual fund, a professional fund manager pools your money with that of thousands of other investors and invests it across dozens or hundreds of stocks, bonds, or other assets. Your returns reflect the portfolio's collective performance.

This single structural difference drives almost every other distinction between the two options.

Mutual Funds vs Stocks: A Direct Comparison

What Are the Risks of Investing Directly in Stocks?

Starting direct stock investing is not difficult. It is difficult to make a profit without the right skills and time.

SEBI's July 2024 study on intraday trading found that 7 out of 10 individual intraday traders in the equity cash segment lost money in FY2022-23. Loss-making traders spent an additional 57 per cent of their trading losses on transaction costs alone.

The numbers are worse in derivatives. SEBI's September 2024 F&O study found that 93 per cent of individual equity F&O traders incurred losses between FY22 and FY24. Aggregate individual losses across those three years exceeded ₹1.8 lakh crore.

These figures cover active traders, not long-term investors. But they make one thing clear: the stock market heavily rewards those with time, information, and emotional discipline, and penalises those without it.

What makes direct stock investing hard?

Three things trip up most retail investors:

- Stock selection. Identifying which companies will outperform requires reading financial statements, tracking sector trends, and understanding competitive dynamics. Most investors underestimate this effort.

- Portfolio sizing. Knowing how much to allocate to each stock is a separate skill from picking the stock itself.

- Emotional discipline. Holding through a 30 to 40 per cent drawdown without panic-selling is harder in practice than in theory. Most investors exit at the worst possible moment.

What Are the Advantages of Mutual Funds Over Direct Stocks?

Professional Management

Fund managers and their research teams analyse companies full-time. That is their only job. A salaried professional cannot replicate this attention between work, family, and everything else.

Diversification at Low Cost

A single equity mutual fund may hold 40 to 80 stocks. Building equivalent diversification directly would require significant capital and ongoing rebalancing. A SIP of ₹5,000 a month buys into a professionally managed, diversified portfolio from day one.

Rupee Cost Averaging via SIP.

SIPs invest a fixed amount every month regardless of market levels. When markets fall, the same ₹5,000 buys more units. When markets rise, it buys fewer. Over time, this averages out the cost per unit and reduces the impact of market timing errors.

Low Minimum Entry

Most equity mutual funds accept SIPs starting at ₹500 per month. Buying a meaningful position in a quality large-cap stock directly often requires significantly more capital upfront.

No Tax on Internal Rebalancing

When a fund manager sells one stock and buys another inside a mutual fund, you pay no tax on that transaction. The tax clock only starts when you redeem your units.

If you manage stocks directly, every sell decision is a taxable event. Sell a stock after a year? You pay 12.5% LTCG on the gains. Sell within a year? You pay 20% STCG. These taxes add up fast, especially if you rebalance regularly.

For retired investors with no salary income, this matters even more. A tax bill from portfolio rebalancing has to be paid from somewhere. In a mutual fund, the manager can shift the entire portfolio without triggering a single rupee of tax liability for you.

Regulated and Transparent

All mutual funds in India operate under SEBI regulation. Fund houses publish daily NAVs, monthly portfolio holdings, and audited financial statements. Investors know exactly what they own.

For a concise breakdown of how these advantages play out in practice, see FinAtoZ's earlier piece on the 5 advantages of mutual funds over stocks.

Which Type of Mutual Fund Should You Choose Instead of Stocks?

Not all mutual funds behave the same way. If you are moving away from direct stocks or considering mutual funds as an alternative, the category you choose matters.

Large-cap funds invest in the top 100 companies by market capitalisation. They are less volatile and suit investors who want equity exposure without the swings of mid- or small-cap stocks.

Flexi-cap funds give fund managers the freedom to move between large, mid, and small-cap stocks depending on market conditions. They suit investors with a 7-year or longer horizon who want a single, actively managed equity fund.

Index funds passively track an index such as the Nifty 50 or Sensex. They carry no fund manager risk, have the lowest expense ratios among equity funds, and are increasingly recommended as a starting point for first-time investors.

Small-cap and mid-cap funds carry higher volatility. They can significantly outperform over 10-year-plus periods but require the discipline to hold through sharp drawdowns. They are not a substitute for the excitement of direct stock picking. They are long-term compounding tools for patient investors.

If you are unsure which category fits your goals and risk profile, a certified financial planner can map these options to your specific situation before you invest.

When Does Investing Directly in Stocks Make Sense?

Direct stock investing suits investors who meet specific conditions. It is not a universal upgrade from mutual funds.

It makes sense when:

- You have the time to research companies and monitor your portfolio regularly, typically several hours a week.

- You have enough capital to build a diversified portfolio of at least 15 to 20 stocks across sectors.

- You have experience reading balance sheets, profit and loss accounts, and cash flow statements.

- You can hold positions through significant drawdowns without making emotionally driven decisions.

If all four apply, direct stocks offer two advantages that mutual funds cannot match: no fund management fees, and the ability to concentrate capital in your highest-conviction ideas.

If even one of the four is missing, the structural advantages of a mutual fund almost always outweigh the potential gains from stock-picking.

How Should Your Goal and Timeline Influence the Decision?

The stocks vs mutual funds question rarely has a universal answer. It almost always depends on what you are investing in and how long you have to invest.

Short goals (under 3 years): Neither direct stocks nor equity mutual funds are appropriate for short-term goals. Market volatility over short periods can erode capital at precisely the wrong moment. Debt mutual funds, fixed deposits, or liquid funds are better suited here.

Medium-term goals (3 to 7 years): Balanced advantage funds or hybrid mutual funds that dynamically adjust equity and debt allocations are a reasonable option. Direct stocks in this window carry significant timing risk.

Long-term goals (7 years and beyond): Here, equity mutual funds and direct stocks both perform well. The difference comes down to time and skill. If you have both, stocks can work. If you have one or neither, equity mutual funds through SIPs are the more reliable vehicle for compounding over the long run.

Aligning your investment choice to your goal timeline is the foundation of financial planning. It is also the step most self-directed investors skip.

If you have not yet mapped your goals to a timeline, start there first. Understanding the difference between short-term and long-term financial goals will shape every investment decision that follows, including this one.

Mutual Funds vs Stocks: Tax Treatment in India

Both direct equity investments and equity mutual funds attract the same capital gains tax rates in India as of FY2024-25:

- Short-term capital gains (STCG): 20 per cent, applicable if equity is sold within 12 months.

- Long-term capital gains (LTCG): 12.5 per cent on gains exceeding ₹1.25 lakh per year, applicable if held for more than 12 months.

Debt mutual funds do not receive indexation benefits and are taxed as per the investor's income tax slab for units purchased after April 1, 2023.

Tax treatment is one area where stocks and equity mutual funds are now on equal footing. The decision should be made on skill, time, and temperament, not tax efficiency.

How FinAtoZ Approaches This Decision

FinAtoZ is a SEBI-registered investment adviser (INA200006628) and a fee-only firm. It earns no commissions from any mutual fund house or financial product. Every recommendation is made in the client's interest, not in the interest of a distribution margin.

Its investment selection process runs through a proprietary 4P1R Research Process that evaluates funds across five dimensions before recommending them to clients. This process applies regardless of market conditions or fund popularity.

For clients who are genuinely suited to direct stock investing, FinAtoZ does not push mutual funds as a default. For clients who are not, it does not recommend stocks to appear sophisticated. The distinction matters because most firms that sell financial products have an incentive to recommend whatever pays them more. A fee-only adviser has no such incentive.

You can start a conversation with a FinAtoZ CFP through a no-obligation introductory call.

Frequently Asked Questions

Which gives better returns: mutual funds or stocks?

Direct stocks have the potential to deliver higher returns than mutual funds, but only for investors who select well, diversify properly, and hold through volatility. For most retail investors, the consistency of a well-chosen equity mutual fund held via SIP over 10 or more years outperforms the average outcome of direct stock investing.

Can I invest in both mutual funds and stocks at the same time?

Yes. Many experienced investors hold a core mutual fund portfolio for long-term goals and a smaller direct equity portfolio for conviction-based bets. The mutual fund portfolio provides stability and discipline. The direct equity portfolio provides upside for those willing to do the work.

Is a SIP in mutual funds safer than buying stocks?

SIPs in equity mutual funds are still subject to market risk. They are not guaranteed. What SIPs reduce is the risk of mistimed entry, as you invest through both high- and low-market phases. They also reduce the risk of poor stock selection, because a fund manager makes those decisions. Neither risk disappears entirely.

How much money do I need to start investing in mutual funds?

Most equity mutual funds in India accept SIPs from ₹500 per month. There is no minimum for lump sum investments in most funds, though many advisers recommend a minimum of ₹5,000 for a lump sum to be meaningful.

What is the difference between a mutual fund and the stock market?

The stock market is the exchange where shares of individual companies are bought and sold. A mutual fund is a pooled investment vehicle managed by a professional that invests in the stock market (and other asset classes) on behalf of its investors. Buying a mutual fund means participating in the stock market indirectly, with built-in diversification and professional management.

Related Reading

Get Expert Financial Advice

Book an introductory call with our Certified Financial Planner to explore how we can help you achieve your financial goals.

Book Your Appointment