Fixed Deposits vs Mutual Funds: A Comparative Analysis

Thanks to the increasing financial awareness among people, they're actively looking to invest for the future. The priority is to generate wealth with strong control over risk, and in the shortest time possible.

Ticking both boxes, two options stand out for them in the present-day financial markets: Fixed Deposits (FDs) and Mutual Funds. They're confronted with the comparison: FD vs Mutual Funds.

Both modes of investment have their merits and demerits. Both options have minimal risks associated with them. It ultimately depends on the investor to choose one of them. But before taking the step, knowing what they are and having clarity on FD vs Mutual Funds is necessary to make a better choice.

FD vs Mutual Funds in Finance: The Basics

Fixed Deposits: What They're

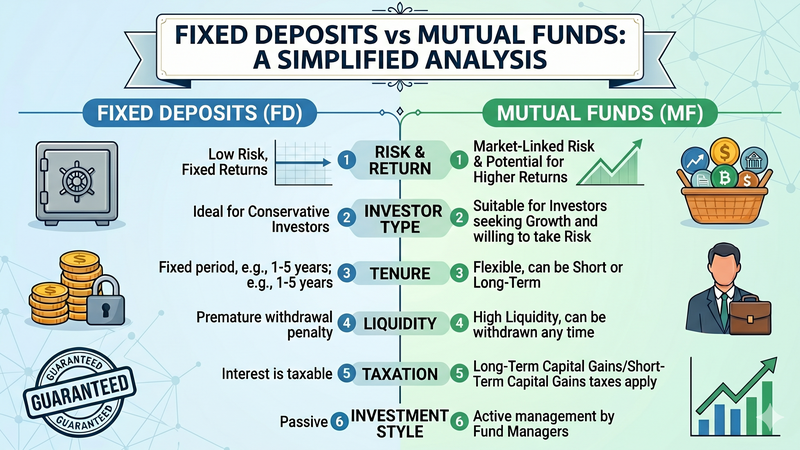

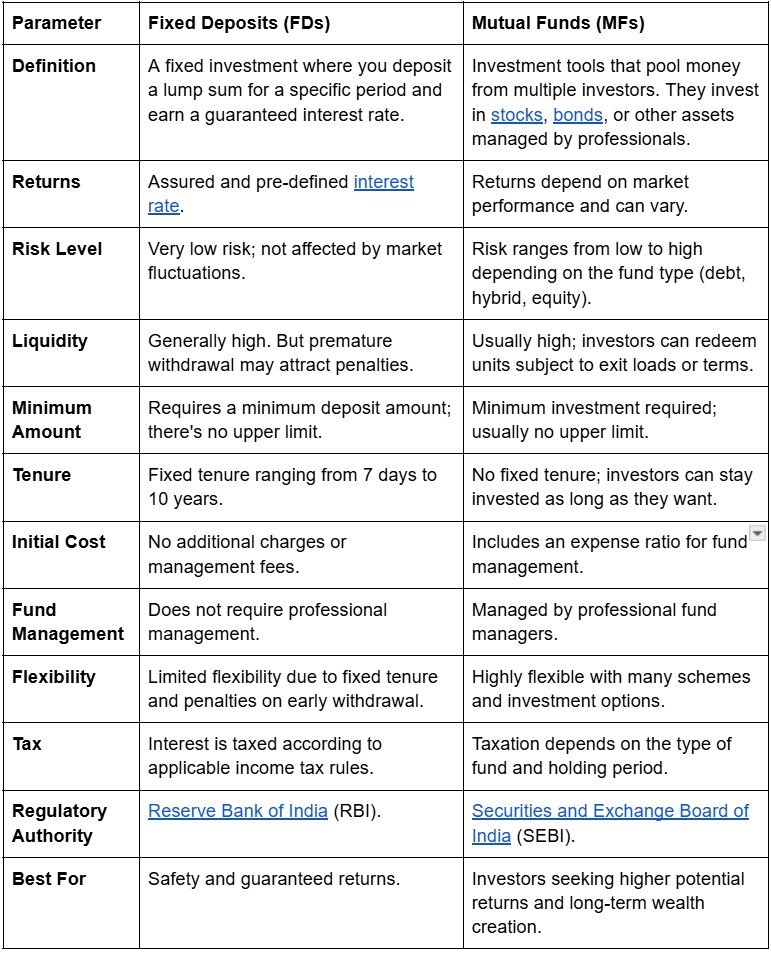

Fixed deposits (FDs) are the most traditional and secure form of investment for wealth creation. As the name suggests, fixed deposits work based on fixed interest rates. They're usually offered by scheduled banks in India with various interest rates, based on RBI interest rates. Investors park a lump sum for a fixed tenure.

They draw a fixed interest throughout the period based on the interest rate. FDs are not linked to the market. It makes them the most reliable investment for risk-averse individuals. While interest accrues over time, the interest rate is further compounded, generating more returns. However, generating wealth through FDs is more beneficial when a larger sum is invested.

Example

Suppose an investor deposits ₹1,00,000 in an FD for 5 years at an interest rate of 7% per annum. At the end of the tenure, the investment grows steadily with compounded interest, and the investor receives the principal amount along with the accumulated interest. Regardless of market conditions, the returns remain fixed and predictable.

Mutual Funds: What to Expect

Mutual funds are market-linked investment instruments that allow investors to participate in a diversified portfolio without directly managing individual securities. Money from multiple investors is pooled together. It is invested in assets like stocks, bonds, and government securities.

These investments are managed by professional fund managers. They make strategic decisions based on market research, economic trends, and the fund’s investment objective. The performance of a mutual fund depends on how well these underlying assets perform in the market.

One major difference between an FD and a mutual fund is that the latter does not offer guaranteed returns. But they have the potential to generate higher returns over the long term, e.g., when invested in equity-oriented funds.

The level of risk varies depending on the type of fund chosen. Debt funds generally carry lower risk, while equity funds involve higher market exposure.

Mutual funds also have flexibility in investment methods. Investors can invest a lump sum amount or choose a Systematic Investment Plan (SIP), which allows them to invest smaller amounts at regular intervals. This makes mutual funds accessible to a wide range of investors with different financial goals and risk appetites.

Additionally, mutual funds provide diversification, i.e., the invested money is spread across multiple assets. It reduces the impact of poor performance from any single investment.

Example

Suppose an investor starts a SIP of ₹5,000 per month in an equity mutual fund. The fund invests this money in different company stocks. Over time, if the stock market performs well, the value of the investment may grow significantly.

For instance, a monthly SIP of ₹5,000 invested for 10 years in a fund delivering an average annual return of 12% could grow to a substantially larger amount than traditional savings options.

FD or Mutual Funds: Which One Is Right for You?

When comparing a mutual fund vs. a fixed deposit, the right choice depends on your financial goals, risk tolerance, and investment horizon.

Fixed Deposits

- Risk-averse investors who prefer capital protection over higher returns.

- Senior citizens looking for a stable and predictable income.

- Short-term investors who want to park their money safely for a fixed period.

- Investors seeking guaranteed returns without exposure to market fluctuations.

- Individuals who prefer simple and straightforward investment options without active monitoring.

- People saving for specific short-term goals, such as emergency funds or upcoming expenses.

Mutual Funds

- Investors seeking higher returns than traditional savings instruments.

- Individuals with moderate to high risk tolerance who are comfortable with market fluctuations.

- Long-term investors aiming to build wealth over time.

- Young professionals and salaried individuals who want to invest regularly through Systematic Investment Plans (SIPs).

- Investors looking for diversification, as mutual funds spread investments across multiple assets.

- People who prefer professional fund management rather than managing investments themselves.

Frequently Asked Questions

Which is the best, an FD or a mutual fund for safety?

Yes. Fixed deposits are considered safer because they offer guaranteed returns and are not affected by market fluctuations. Mutual funds are market-linked investments, so their value can rise or fall depending on the performance of the underlying assets.

Can I lose money in mutual funds?

Yes, it is possible. Mutual funds invest in market instruments like stocks and bonds, so returns are not guaranteed. Short-term market volatility may cause temporary losses, but long-term investments often reduce this risk.

What is the difference between an FD and a mutual fund?

The main difference between an FD and a mutual fund lies in returns and risk. Fixed deposits provide guaranteed interest with low risk, while mutual funds are market-linked investments that can offer higher returns but come with varying levels of risk.

Fixed deposit or mutual fund, which is better?

Mutual funds generally have higher return potential over the long term because they are market-linked. Fixed deposits provide stable but comparatively lower returns since their interest rates are fixed and not linked to market growth.

Can beginners invest in mutual funds?

Yes. Beginners can start with small amounts through Systematic Investment Plans (SIPs). Many investors begin with diversified equity or hybrid funds, which are managed by professional fund managers and designed for long-term wealth creation.

Get Expert Financial Advice

Book an introductory call with our Certified Financial Planner to explore how we can help you achieve your financial goals.

Book Your Appointment