NRE vs NRO vs FCNR Accounts: What Dubai NRIs Must Know

Arjun has been in Dubai for six years. He earns well, sends money home regularly, and has, according to his CA, "all the right accounts set up." What his CA never explained is that Arjun has been routing a portion of his AED salary into his NRO account and losing 30% of that interest to TDS every single year. Not because of any rule he broke. Because nobody told him which account does what.

NRE, NRO, and FCNR accounts are not interchangeable. Each one serves a specific purpose, carries a specific tax treatment, and belongs in a specific part of your financial life as a Dubai NRI. Route the wrong income into the wrong account, and you either hand the government money you did not owe, or you lock yourself out of repatriation when you actually need it.

Here is exactly how each account works, and how to use all three without making Arjun's mistake.

What Is an NRE Account and Why Do Dubai NRIs Use It Most

Your NRE account is where your foreign earnings belong. When your AED salary comes in, the bank converts it to Indian rupees at the prevailing exchange rate and credits the balance. The interest you earn on that amount is not taxable in India. Zero TDS.

More importantly, every rupee sitting in an NRE account is fully repatriable under RBI regulations, principal and interest, with no annual cap. You can move it back to your Dubai account whenever you choose, without filing extra paperwork or seeking RBI permission.

What most comparison articles skip: you can fund Indian mutual fund SIPs directly from an NRE account. This matters because investments made from NRE funds retain their repatriable character. The wealth you build in India stays fully accessible from Dubai. If you are doing any long-term goal-based investing built around a research-backed process, routing through NRE keeps your options open without any compliance headache later.

One limitation worth knowing. The NRE account holds rupees. If the rupee weakens significantly against the dirham, the value of your deposit in AED terms shrinks. For short-term parking of salary before it gets invested, that is fine. For large lump sums you may need back in foreign currency, read the FCNR section below.

What Is an NRO Account and When Do Dubai NRIs Actually Need It

The NRO account is for income that originates in India. Rent from your flat in Pune. Dividends from Indian stocks. Pension payments. Interest from old fixed deposits. All of that goes here.

The mistake I see most often: Dubai NRIs treat the NRO account like a general-purpose Indian account and start crediting foreign salary into it. The moment you do that, the income becomes taxable. Interest on NRO balances is subject to 30% TDS, and repatriation from NRO accounts is capped at USD 1 million per financial year, after taxes and documentation are cleared.

Priya's CA called her in March with a simple question. Had she checked which account her salary was going into. She had not. Two years of AED deposits sitting in NRO, taxed at 30% each time interest accrued. Your NRO account is not a general account. It holds what India pays you. Rent from a property. A dividend that hit your demat. Nothing from Dubai belongs here, and mixing the two does not just cost you tax. It complicates every repatriation you try to do later. If you ever want to shift NRO balances across to your NRE account, the tax has to be settled first, and the amount sits inside your annual outward limit.

Managing Indian rental income, dividends, or any other India-sourced earnings? The financial checklist for NRIs investing back in India covers how to structure repatriation correctly once you are ready to move funds.

What Is an FCNR Account and Why Is It the Smartest Play When the Rupee Is Weak

Ask ten Dubai NRIs about their FCNR account. At least seven will go quiet. This is the one worth paying attention to if you are sitting on a lump sum in foreign currency and are not certain when you are returning to India.

An FCNR deposit lets you hold a fixed deposit in India in a foreign currency, such as USD, GBP, EUR, or AED. The deposit stays in that currency. It does not convert to rupees. Neither the interest nor the deposit amount is subject to tax in India, and you can transfer all of it back to your overseas account without exceeding any annual ceiling.

Here is the specific advantage for the Dubai NRI. If the rupee slips 3 to 4% in a year, your money sits in an NRE account, your AED-equivalent balance shrinks by that much. An FCNR deposit in USD or AED holds its foreign currency value regardless of what the rupee does. For someone who cannot pin down a return date, this is the account that buys you time without bleeding value.

FCNR deposits run from one to five years. Premature withdrawal attracts a penalty, so do not park money here that you might need at short notice. If you have savings sitting beyond your regular NRE balance and your return is still a few years out, talk to an advisor who handles NRI retirement and wealth planning before you decide.

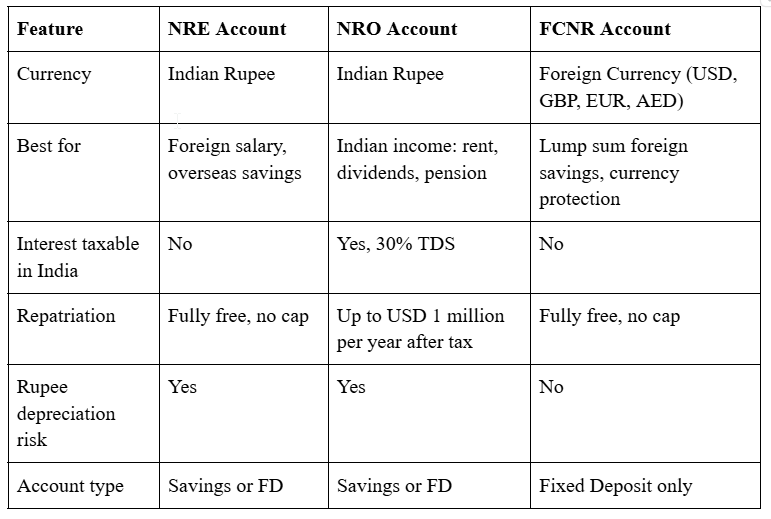

NRE vs NRO vs FCNR: A Side-by-Side Comparison for Dubai NRIs

Most guides give you a generic table. This one is built specifically around the questions Dubai NRIs actually ask.Your AED salary goes into NRE. Indian rental income sits in NRO. Got a lump sum in foreign currency with no fixed return date? That is what FCNR is for. Where people go wrong is using one account for everything. The NRO feels familiar so it becomes a catch-all, and that is exactly how unnecessary TDS accumulates. If you are also managing overseas retirement savings alongside these accounts, the guide on what happens to your savings when you move back to India covers how to coordinate them.

Conclusion

For most Dubai NRIs, the account structure is not complicated once the logic is clear. Foreign salary is treated as NRE and remains tax-free and fully repatriable. Indian income is deposited in NRO and managed separately. Large lump sums that require currency protection are placed in FCNR.

The real cost of getting this wrong is not a fine. It is years of unnecessary TDS, repatriation delays, and a scramble to fix account classifications right when you are trying to plan a return.

If you are not certain that your current account structure is set up correctly, the most useful starting point is a single advisory session with someone who has specifically handled NRE, NRO, and FCNR structuring for Dubai-based clients. Book a conversation with the FinAtoZ team to review your current setup and confirm that everything is working as it should.

Frequently Asked Questions

My CA said to open all three accounts. Do I actually need all of them?

Not necessarily, and this is where many Dubai NRIs end up overcomplicating things. Whether you need all three depends entirely on your income sources. If your only income is your AED salary and you have no property or investments generating income in India, an NRE account alone covers most of what you need. The NRO account becomes necessary the moment you have Indian-sourced income, rent, dividends, or a pension, because that money cannot be deposited directly into an NRE account. FCNR only makes sense if you have a lump sum in foreign currency that you want to park safely for one to five years without converting it to rupees. Open accounts based on what your money is actually doing, not because someone told you to have all three.

I am returning to India next year. What do I do with my NRE account before I leave Dubai?

Convert it to a resident savings account or RFC account as soon as you return. Your bank will expect this within 30 to 90 days of your arrival. If you have NRE fixed deposits running past your return date, check the maturity dates now, because interest that accrues after your status changes is no longer tax-free in India.

Can I invest in Indian mutual funds directly from my NRE account?

Yes. Investments made from an NRE account are treated as repatriable investments, meaning the proceeds can be sent back abroad without being blocked by the NRO repatriation cap. You will need to update your KYC with the fund house reflecting your NRI status. SIPs funded from NRE accounts let Dubai NRIs build an India portfolio that stays fully repatriable, so the wealth you create here does not get trapped when you need it abroad.

Is the interest earned on an FCNR deposit taxable in the UAE?

The UAE currently has no personal income tax on investment income, so FCNR interest is not taxable at the UAE end either. In India, FCNR interest is exempt from tax for NRIs under the Income Tax Act. This makes FCNR one of the few instruments where your deposit grows completely free of tax at both ends, as long as your NRI status is maintained.

I receive rental income from a property in India. Which account should it go into?

Rental income earned in India must go into an NRO account. It cannot be credited directly to an NRE account. The income is subject to TDS in India. Once it is in your NRO account, you can repatriate it to your Dubai account within the USD 1 million annual limit, provided you have completed the required tax documentation. Keep your NRE and NRO accounts strictly separated so foreign salary never mixes with Indian-sourced income.

Get Expert Financial Advice

Book an introductory call with our Certified Financial Planner to explore how we can help you achieve your financial goals.

Book Your Appointment