Monthly Update - Apr & May 2018

Current market condition can be understood better if we analyse the following factors:

- Improving Micros - Corporate earning is improving steadily over the last four quarters. It has improved by around 11% from the year-ago period. Most of the analysts expect this momentum to continue and earnings are projected to grow steadily over the next 2 to 3 years.

- Worsening Macros - There are some key macro factors that have not been doing good for the last few months. Notable among them are soaring crude oil prices, expectation of future rate hikes by US Fed and depreciation of rupee which is increasing the trade deficit.

- Re-categorisation of Mutual Funds - This factor has impacted the stock markets in India in the last 2 months. And may continue to have some impact in the next 1 month or so. Since SEBI has mandated all the Mutual fund companies to re-categorise their existing funds and make changes in the existing portfolio accordingly, it has resulted into a significant short term churn in the industry. This churn has lead to a temporary under-performance particularly in the mid and small cap funds.

Going forward, our view is that there is a very low probability that the macros will worsen further from here. Crude oil prices have gone up with a temporary cut in production from top oil manufacturers like Saudi Arabia and Russia. With the prices having risen now, there is a good chance that they may start increasing their productions. Moreover, US Oil shale production becomes viable at around $65 per barrel. So, it very unlikely that the crude oil prices can rise much beyond these levels. Similarly, some part of the rate hikes by the US Fed is already factored in the stock and bond prices. So, this factor though negative is unlikely to be a major spoilsport.

Hence, in our view, the equity markets are placed in a way which balances out the negatives with the positives. Hence it may continue to trend sideways for sometime before it takes a definite direction again.

Our view on other asset classes:

- Equity - Neutral

- Debt - Slightly positive (The yields have risen substantially in the anticipation of rate hikes by RBI. Hence, debt especially the corporate debt looks slightly positive now)

- Gold - Neutral

- Real Estate - Slightly negative

In the current market conditions, it is best to maintain your respective asset allocation and ride the markets with disciplined investing via SIP.

MACROECONOMIC TRENDS

Kindly refer to the below graphs for a summary of major macroeconomic parameters and their respective trends:

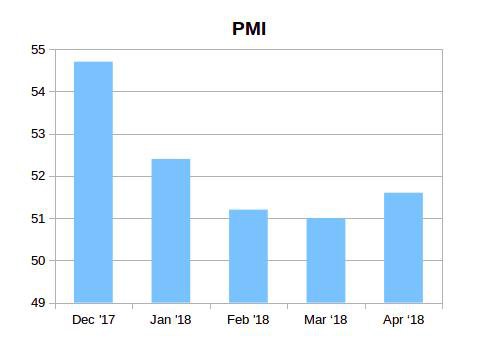

PMI

PMI India increased to 51.6 this month from 51.0 last month. This is greater than the market expectation of 51.3.

INFLATION

Inflation in India has increased 4.58% than 4.28% in the previous month and above the market expectations of 4.42%.

TRADE DEFICIT

Trade deficit has widened to $13.72 billion in Apr'18 as compared to $13.25 billion a year earlier. It is lesser than the market expectations of $15 billion.

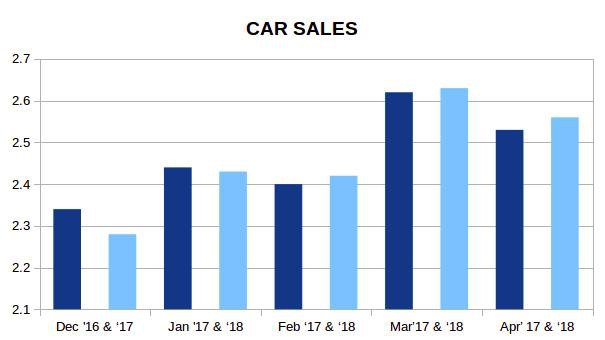

CAR SALES

Car Sales has Increased by a marginal rate of 1.19% year-on-year last month.

CORPORATE EARNINGS

Overall the trend for corporate earnings looks to be upward from last few quarters. It is the highest since Q2 16-17

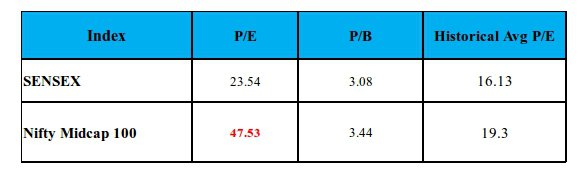

VALUATION

Mid Caps and Small Caps continue to be over-valued as per historical averages. Large caps are comparatively much better placed at the moment.

Get Expert Financial Advice

Book an introductory call with our Certified Financial Planner to explore how we can help you achieve your financial goals.

Book Your Appointment