How we choose best mutual funds for your portfolio?

"Mutual fund sahi hai" is true only if you select the right one :) Many investment advisers will argue that mutual fund selection is an art. We, however, believe that it is more of a science. With our many years of investment experience, we have tried to master the science of mutual fund selection process for our customers. We use sophisticated analytical tools like Morningstar Research Workbench and FE Analytics for our analysis. The process is repeated every quarter or if there is a trigger to re-evaluate (whichever is earlier). This article is our endeavor to explain the mutual fund selection process at FinAtoZ in detail.

Mutual fund selection process @ FinAtoZ

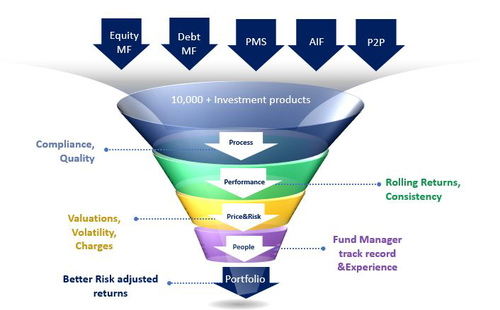

Core of the mutual fund selection process at FinAtoZ is what we call the 5P methodology! 5P stands for Process, Performance, Portfolio, People & Price.

You can read more about the fund selection methodology at FinAtoZ Research Methodology.

The Big Filter

There are more than 10,000 mutual funds in the market. It does not make sense to analyse all the 10,000+ funds on all the investment parameters. So, the first step is to filter-out "below average performers". This will result into a shorter list for deep-diving. The filter is created for each category separately. For example, we filter-out below average funds separately for large-cap and mid-cap mutual funds.

Lets try to understand how the filter is created. We have the following parameters as filter:

1. Fund Size

Funds with a relatively smaller size generally don't get the requisite management bandwidth. This is because a small fund may not be profitable for the asset management company. Hence, they may not be interested to put their best resources to manage the funds with smaller size.

Next question is what size is considered to be decent enough. Size varies for each category of mutual fund. For example, if we want to create a filter for large-cap mutual funds, we may filter out all mutual funds with less than 5000 Cr fund size. However, for a small-cap mutual fund, we may consider all funds with more than 1000 Cr fund size.

Another interesting point to note is that funds with a very large size may also not be good. This is because it is not easy to manage very large funds. Moreover, the choice of stocks for the fund manager gets limited. For instance, a fund has a size of 30,000 Cr. Now, to add a stock to this fund's portfolio, it should have a very large market-cap. Else, it will not be possible for the fund manager to add that stock in the portfolio. Hence, we also filter out funds which are very large is size.

2. Past Performance

Second filter is to weed out funds based on their past performance. We generally consider 5 year performance for this filter. We filter out funds which could not even match the average performance for their respective category. The recent MF categorization done by SEBI comes in handy for us to create a performance filter for each Mutual Fund category.

3. Volatility

Third filter is the volatility (or the standard deviation) of the fund. We further filter-out funds that have higher volatility than the mean of each category. Essentially, we don't want to invest in funds that show rapid short term movement in either direction. Idea is to avoid funds that have shown good performance just because of some short-term spike. We want to invest into funds that show much better consistency.

The Deep Dive

The Big filter results into a list of around 10-15 mutual funds in each category. All the noise is filtered out and we are ready to do the real job on hand. We then carefully analyze the mutual funds on the 5P parameters as detailed below:

Let’s understand the mutual fund selection process in detail with the help of an example. We have taken the analysis of small cap as an example.

1. Process

The first "P" includes the process followed at each Asset Management Company. What is their process for stock selection? How has been their past consistency? Do they comply with SEBI guidelines? etc. Robust stock selection and management process ensures that there is a minimal impact from an unpredictable event in the company.

Total Asset Size - There are several factors that are considered to evaluate the robustness of the "Process" at a particular fund house. Total asset size of a fund house is one of them. Fund houses with large asset size can afford a more qualified and a larger team to manage their funds. Thus they have the resources to build strong processes. Smaller companies process may not be robust enough. Any small change affects the whole functioning of the company. For example, there could be a huge impact if the CEO of a small asset management company leaves.

Stock selection methodology - Another important check-point is the stock selection methodology deployed at the fund house level. Do they have a team of internal financial analysts tracking each sector? Or do they buy research reports from external sources? What is the dependency on the fund manager or the CIO of the company? Answer to these questions give us a fair idea about the robustness of the internal process at a particular asset management company.

2. Performance

Performance has multiple facets. What is often visible at the first look may not reveal the real picture. If one looks at past performance, it may give a distorted picture. This could be due to recent out-performance or under-performance. What is probably more important is the consistency of the return. What is also important is the risk that has been taken to generate a particular kind of return. Often people overlook the risk parameters and focus only on the returns.

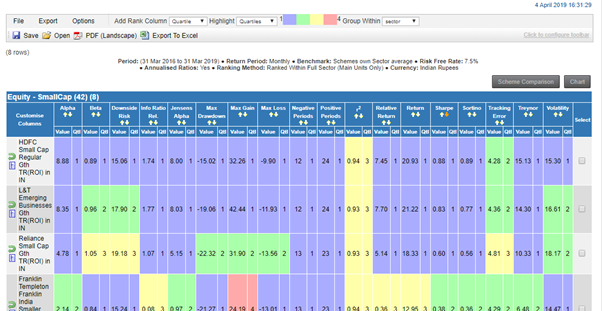

We look at the following performance ratios for evaluation:

Risk adjusted return (Sharpe ratio) – It is the most widely used method of risk-adjusted returns. It helps to understand the return of an investment compared to the risk. The Sharpe ratio is the average return earned in excess of the risk-free rate per unit of total volatility. In simple words, the Sharpe ratio is the additional return an investor is getting for the additional risk he/she is taking compared to a risk-free asset like FD. The higher ratio represents higher returns for every unit of risk.

Downside Risk – Downside risk is an estimation of a fund's potential to suffer a decline in value if the market conditions change. Downside risk explains a worst-case scenario for an investment or indicates how much the investor stands to lose if markets go down. Evaluating the downside risk helps us to avoid focusing only on performance. Investments with lesser chance of downside risk may have a greater potential for overall positive returns.

Volatility – It is the amount of uncertainty or risk related to the changes in an investment’s value. If the volatility is higher the price of the asset can change significantly in the short term in either direction. Lower volatility means the price of the investment doesn’t fluctuate much in the short term and tends to be steadier. To put it simple, it is the measure of sudden price movement.

Here, for ex. HDFC Small Cap’s & L & T emerging businesses’ ratios are good. Both the funds show up in top 5 small-cap funds in our analysis. On deeper analysis, when we analyze the rolling returns (explained below), the situation changes. HDFC Small Cap fund moves down and L&T emerging businesses fund comes at top of the chosen list.

The above three ratios helps us to further down-select top 5-7 funds for each MF category. Ratios for 3 years and 5 years are considered in the above analysis.

Lets understand the next steps of the mutual fund selection process:

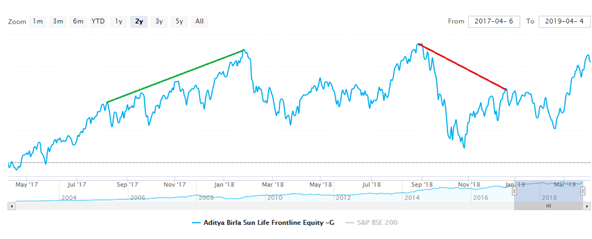

Rolling Returns – We need to consider the consistency of the fund in all market cycles. So, we compare the performance of the fund with the its historic overlapping cycles / time periods.

Rolling return is the measure of the same. Absolute and annualized returns only consider the beginning value and the end value. It doesn’t consider what happened in the investment period. They can also get manipulated by taking the wrong starting and end period. Based on the time period taken it can show a positive or negative picture. We need to move the time period in definite intervals and see the returns in all the different time periods. It is more accurate and not biased to a particular period.

Ex: Lets consider the performance of ABSL Frontline Equity Fund. If we check the below time periods in the chart below, we observe the following:

- Jul 17 to Dec 18: returns are positive and looks very good.

- Aug 18 to Jan 19: returns are negative and looks ugly.

Based on this information will it be possible to conclude whether this fund is worth investing? What is missing in this analysis? Lets try to understand more:

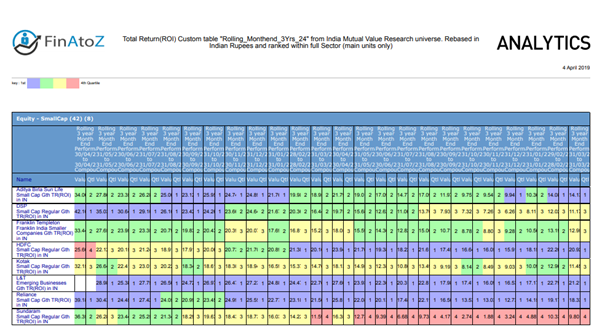

Rolling returns offers better insight into a fund's more comprehensive return history, not skewed by the most recent data (month or quarter-end). Rolling returns enables our research team to check the performance of the fund in multiple time periods within an overall time-frame. For instance, if we want to analyze 5 year return history of the above fund, we can break it into 36 time periods of 3 year returns. For example, Jan-2014 to Dec-2016 is one time period. Similarly Feb-2014 to Jan-2017 is another period....and so on. So, a 5 year time period from Jan-2014 to Dec-2018 will get divided in at total of 36 periods of 3 years each. We can then analyze whether the fund outperformed the category during each of these periods. Based on this analysis we can choose the funds which have outperformed in most of the time period across the market cycle (generally last 5 years).

Example: In the below study, L&T emerging businesses have outperformed the category in all the market cycles.

After analyzing the rolling returns, we choose the best 4 or 5 funds which performed well most all the market cycles.

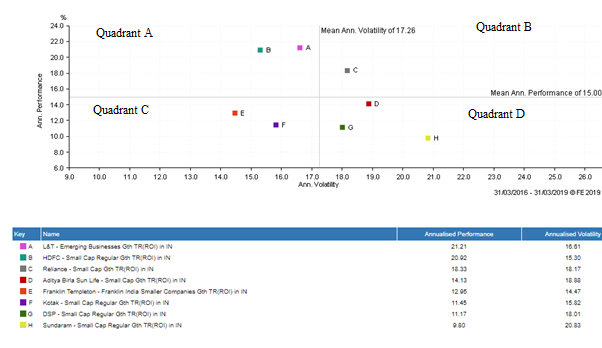

Risk / Return Quadrant – Another factor which we consider in our mutual fund selection process is the risk-adjusted returns. One of the key factors to choose funds is to take a lower risk and get higher returns than average. To get the average, we calculate the average returns and risk (Standard Deviation) for all the funds of a given category. For example in the below scatter chart of small-cap funds there are 12 products. The average returns are 15% and the average risk is 17. Using these two averages the four quadrants are prepared.

- Quadrant A is less volatile and returns are high

- Quadrant B is both high on volatile as well as returns

- Quadrant C is less volatile and low returns

- Quadrant D is highly volatile and low returns.

Ideally, funds which fall under quadrant A are the best as they are less volatile, and returns are high. We can also look at quadrant B for aggressive investors. They are ready to take additional risks for want of higher returns. Quadrant C is suitable for a risk averse customer who wants capital to be preserved as a top priority. Quadrant D is the worst as it has high volatility and low returns. This quadrant should be avoided completely for all types of customers. In the below chart we can see L&T emerging businesses falls under Quadrant A in which returns are higher than the mean and volatility is lesser than the mean.

3. People

A high-quality management team is another important factor for any investment product to outperform in the long run. There is significant churn in the portfolio management industry. So it is important to keep a track of the changes in the management team of each investment product.

Fund Manager Performance – A fund manager is responsible for implementing the investment strategy and portfolio management. He picks the stocks, bonds or other assets for the fund. He is the one who is strategically managing the fund. He takes call to deploy investor’s money. A fund manager should ensure that the fund gives consistent returns within the stipulated risk. He should monitor the market, economic trends etc. to give the best results. We like fund managers who outperform the benchmark consistently. Another important factor is to check their performance as compared to their peers. We do a thorough qualitative analysis of fund manager performance. What is their experience in handling the assets and liabilities? How is their performance compared to the peers? How they managed the volatility? How they performed in the rising markets and falling markets? and many more….

4. Price

Price is what we are pay for a particular investment product. Even for personal product like garments, handset etc. price is a very important factor. Hence, it is important to ensure that we pay a reasonable price for any investment product that we invest in. Following factors enable us to evaluate the fair price of an investment product:

Margin of safety – More the price that we pay for an investment product, the lesser the margin of safety. We try to avoid products that are over-priced at a particular time point. We would rather wait for the price to correct and come within our comfort zone. Investing into products which are under-valued ensures that the downside risk is limited and the hard earned money of our investors doesn't get subjected to undue risk.

Management cost – Each investment product has an underlying management cost associated with it. We ensure that the management costs are justified and in line with the performance of a particular investment product.

Cost of exit – Some investment product charge an exit load if one needs to withdraw the investments before the stipulated time. For most of the equity funds the exit load is 1% if redeemed within one year of investments. But some funds put a higher time-frame as well. We ensure that we don't get stuck with an investment product for a long period of time. We should be free to change the investments if a particular product is not performing well. Or if market conditions changes drastically.

Qualitative Analysis – There are many other important factors that needs to be considered as well. Factors like:

- Any fund acquisition in the past

- Any major fund mandate change

- Any restrictions in taking new money

- The future outlook for the chosen fund category

Qualitative analysis enables us to develop forward vision. It helps us to avoid getting too much entangled with only past numbers.

5. Portfolio

In addition to all these analysis, we customize each investor’s portfolio based on his risk profile, time horizon and goals. Based on the investor’s requirement the portfolio could be a combination of large-cap, multi-cap, small cap, debt etc. We ensure there is not much overlap with the underlying holdings of the chosen funds from each category. Likewise, we consider the investor’s risk appetite and the time horizon of the goal for which the investment is to be done. This is required to get an optimum risk-reward score for the portfolio. Following factors are taken into account to design the final investment portfolio.

Risk profile of an investor – Portfolio creation is based on investor's risk profile. There are three broad categories of investors viz. Aggressive, Moderate and Conservative. Portfolio composition for each category will be different. The investment portfolio is created in such a manner so as to reduce the investment risk. At the same time we try to ensure that it has a minimal impact on the return potential.

Portfolio composition – The investment portfolio comprises of various sectors like large caps, mid caps, credit risk, real estate etc. Care has to be taken to create a proper mix so as to reduce the risk with optimum diversification. When choosing multiple investment products, we need to ensure that there is not much overlap in the underlying holdings of such investment products.

Return potential – The portfolio is created keeping in mind the long term return potential based on prevailing market conditions. Eventually, the investment portfolio should deliver higher return for each unit of risk taken.

Summary

The objective of the entire mutual fund selection process undertaken by us is to put a method to madness. We are cognizant of the fact that we are dealing with hard earned money of our investors. We want to ensure that the entire fund selection as well as portfolio creation process is done in a scientific manner using global best practices.

We believe that our focus on continuous research, analysis and monitoring of portfolio will reduce the investment risk substantially for our clients. We absolutely don't believe in predicting the outcomes of an investment portfolio. Rather we want to create a portfolio which can weather the storm. A sound investment portfolio is one which is deigned as per the investor's risk appetite. Our expertise lies in combining various investment products in such a manner that the total risk of the portfolio is significantly lesser than the sum of individual product risk. At the same time, the portfolio returns are equal to the sum of individual product returns. This is our core investment philosophy. This, if done well on a consistent basis, should lead to a relatively high out-performance over a long period of time.

Get Expert Financial Advice

Book an introductory call with our Certified Financial Planner to explore how we can help you achieve your financial goals.

Book Your Appointment