NRIs living in Dubai can build retirement savings in India through three primary instruments: the National Pension System (NPS), equity mutual funds via NRE accounts, and FCNR fixed deposits.

NRIs living in Dubai can build retirement savings in India through three primary instruments: the National Pension System (NPS), equity mutual funds via NRE accounts, and FCNR fixed deposits. The NPS is the only structured pension plan available to non-residents. Mutual funds offer the most flexibility for long-term corpus building. Both are accessible online, require PAN and NRI KYC, and are regulated by SEBI and PFRDA. Start early; every decade of delay roughly triples the monthly contribution needed to reach the same retirement corpus.

Why Dubai-Based NRIs Face a Retirement Problem Nobody Talks About

There are now 4.36 million Indians living in the UAE. Most live well. Salaries are tax-free, the dirham is pegged to the dollar, and packages often include housing and school fees.

None of that builds a retirement.

The UAE has no pension system for expatriates; instead, there is an end-of-service gratuity capped at two years' basic salary under Article 51 of the UAE Labour Law. An NRI who has spent 20 years in Dubai receives a gratuity of no more than 2 years' basic pay, regardless of salary growth. For most planning to retire in India, this falls well short of what they need.

The other problem is EPF. The Employee Provident Fund stops accumulating the moment you leave India. If you left at 28 and returned at 52, your EPF balance has been frozen for 24 years, earning interest but receiving no fresh contributions.

Closing this gap requires a deliberate plan built around instruments that are available to NRIs, tax-efficient, and denominated in rupees, the currency in which you will spend your retirement.

Related: How Much Do You Need to Retire in India? Use this to calculate your target corpus before choosing instruments.

The Banking Foundation: NRE and NRO Accounts

Before any investment can happen, the right banking infrastructure must be in place.

NRE (Non-Resident External) Account: Funded by money earned abroad and held in rupees. Both principal and interest are fully repatriable. Interest is tax-free in India. This is the primary account for building retirement savings using income from Dubai.

NRO (Non-Resident Ordinary) Account: Holds income earned inside India, rental income, dividends, and interest. Interest is taxable. Repatriation is allowed up to USD 1 million per financial year, subject to applicable taxes and documentation.

For most Dubai-based NRIs, the NRE account is the preferred starting point. Money earned in dirhams goes in, investments flow out into mutual funds or fixed deposits, and accumulated wealth converts smoothly when you return.

Instrument 1: The National Pension System

The NPS is the most overlooked retirement instrument among Dubai-based NRIs, and the only one that functions as a genuine pension, providing not just a corpus but a structured monthly income after you stop working.

NRIs and OCI holders between 18 and 70 can open an NPS Tier I account and contribute from an NRE or NRO account, according to the eNPS platform operated by PFRDA. Funds are invested across equity, corporate bonds, and government securities based on an allocation you choose or allow to shift automatically with age under the Auto Choice option.

At retirement (age 60), you can withdraw up to 60% of the corpus as a tax-free lump sum. The remaining 40% must be used to purchase an annuity from a PFRDA-empanelled provider, paying a monthly income for life. This is what makes the NPS a pension plan rather than just a savings account.

Most Dubai-based NRIs return between the ages of 50 and 60, arriving with a gratuity payment and no ongoing monthly income. An NRI who contributes consistently to NPS for 15–20 years from Dubai will have both a lump-sum corpus and a guaranteed monthly income on return. Fund management charges are among the lowest in India's financial system, making it efficient for long-term accumulation.

If your NRI status changes to OCI after you open the account, specific PFRDA rules govern continued participation. Consult a SEBI-registered investment adviser before opening your NPS account to ensure the structure fits your situation.

Instrument 2: Equity Mutual Funds via NRE Account

Mutual funds are the most flexible instrument for building a retirement corpus. UAE-based NRIs face no FATCA restrictions and can invest with most major Indian AMCs, including HDFC, SBI, Mirae, and Nippon. India's mutual fund industry grew from ₹22.26 trillion in AUM in March 2020 to ₹69.50 trillion by April 2025, according to SBI's NRI investment resource, a more than threefold increase in five years.

Investments must be made in Indian rupees through an NRE or NRO account. The process requires a valid PAN card, NRI KYC (done digitally), a FATCA/CRS declaration, and a linked bank account. Once set up, you can run a monthly SIP directly from your NRE account. Investments made through NRE accounts are fully repatriable.

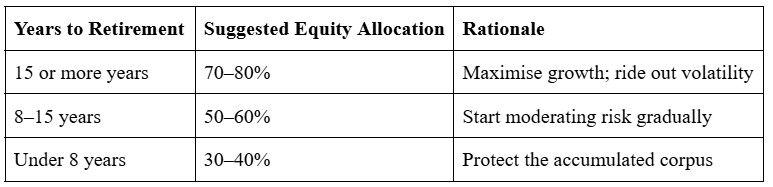

The appropriate allocation depends on your time horizon:

A personalised plan from a certified financial planner will determine the right numbers for your situation.

NRIs pay TDS on mutual fund redemptions, calculated on capital gains. The India–UAE DTAA means tax paid in India is taken into account when computing liability elsewhere. Consult a tax adviser to confirm your position.

Instrument 3: FCNR Fixed Deposits

FCNR deposits allow NRIs to hold fixed deposits in India in their original foreign currency, including USD, GBP, EUR, and AED, with no currency risk during the term. They are capital preservation instruments, not growth instruments, best suited for NRIs within five to eight years of return who want to protect a portion of their corpus from rupee volatility.

Total NRI deposits in India reached USD 161.8 billion as of December 2024, with FCNR deposits alone attracting USD 6.46 billion in April–December 2024, nearly double the year-earlier figure, according to RBI data published by IBEF. As covered in FinAtoZ's piece on the impact of inflation on everyday investments, FCNR deposits protect against currency risk but not rupee inflation, which is why they work best as a complement to equity instruments rather than a replacement.

June 2026 update: the RBI swap window

In June 2026, the RBI reopened a special FCNR(B) swap window to attract foreign currency and support the rupee. Under the scheme, the RBI absorbs the full currency-hedging cost for banks, roughly 3.5%. This lifts the ceiling that normally limits FCNR rates and lets banks pay far more.

Banks moved fast. SBI, HDFC Bank, ICICI Bank, Axis Bank, and Bank of Baroda raised peak FCNR(B) rates to 6% on three-to-five-year deposits, with some lenders going to 7.1% on US dollar deposits, up from around 3.35% earlier. The deposits carry a one-year lock-in. For a Dubai NRI, this is the strongest FCNR pricing in years: close to 6% on a USD deposit with no currency risk during the term.

The leverage angle, and its risk

Brokerages estimate NRIs who use leverage could earn 15% to 27% a year under the 2026 scheme. You place an FCNR deposit through an Indian bank's overseas branch, borrow abroad against it at a low rate, redeposit, and repeat. The gap between the cheap borrowing cost and the higher FCNR rate, multiplied across the leverage, drives the return.

This is an arbitrage trade, not a simple deposit. It depends on borrowing, so it carries margin risk and rollover risk, and the same structure drew systemic-risk warnings after the 2013 version of the scheme. It suits sophisticated investors with professional advice, not a core retirement corpus. Treat the higher headline rate as the retirement-relevant change. Treat leverage as a separate, higher-risk decision.

Get Expert Financial Advice

Book an introductory call with our Certified Financial Planner to explore how we can help you achieve your financial goals.

The Planning Error Most NRIs Make

Dubai-based NRIs typically build their retirement corpus estimate in dirhams, then convert to rupees on the day they retire. The error isn't in the conversion, it's in the timing.

India's retail inflation averaged 5% annually over the decade from 2015–16 to 2024–25, according to Government of India data published by PIB. At 5% inflation, purchasing power halves in roughly 14 years. An NRI who builds ₹3 crore by age 50 and retires at 60 needs to account for what ₹3 crore will actually buy a decade from now — at 5% inflation, approximately ₹1.84 crore in real terms. The corpus that looks sufficient today is materially smaller when it is actually needed.

The correct approach:

- Start with your current monthly expenses in India, not in Dubai.

- Project those expenses forward at 5–6% annually to your target retirement age.

- Multiply the resulting monthly expense by 25–30 to arrive at a corpus target.

- Build your savings target to that inflation-adjusted figure, not today's converted dirham equivalent.

Use FinAtoZ's retirement calculator, built to account for Indian inflation in the corpus projection, to see your real target.

The Two-Portfolio Approach

Portfolio A: Growth (active during working years in Dubai): Invested primarily in Indian equity mutual funds via a monthly SIP from your NRE account. Time horizon: 10–20 years. Target: beat Indian inflation by at least 3–4% in real terms. Primary instruments: diversified equity mutual funds, NPS Tier I.

Portfolio B: Income (built in the 5–7 years before return): Accumulated growth transitions into income-generating instruments, FCNR deposits, debt mutual funds, and NPS annuity. Target: stable monthly income covering 70–80% of projected retirement expenses.

The transition from Portfolio A to B is the step most NRIs delay or miss entirely. Beginning seven years before your target return date reduces the risk of a bad market sequence erasing accumulated gains immediately before retirement.

A Note on PPF

NRIs cannot open a new PPF account. If you had one before becoming an NRI, you can continue contributing until the original maturity date — at which point it must be closed, as NRIs cannot extend PPF accounts the way resident Indians can. Interest is tax-free in India. If your existing account still has years remaining, continuing contributions makes sense as a safe, tax-free addition to your corpus.

Step-by-Step: Building Your Plan From Dubai

- Calculate your corpus target in today's Indian rupees using the FinAtoZ retirement calculator or the benchmarks in How Much Do You Need to Retire in India?

- Open an NRE account, your investment gateway.

- Apply for a PAN card and complete NRI KYC online.

- Open an NPS Tier I account via eNPS on a repatriation basis using your NRE account.

- Set up a monthly SIP in equity mutual funds aligned to your risk profile and time horizon.

- Review the plan annually, not just returns, but your corpus target, return date, and India expenses.

- Begin transitioning to Portfolio B seven years before your planned return.

- Consult a SEBI-registered adviser before major decisions, restructuring on return, converting accounts, or changing NPS fund managers. See also: How to Choose a Financial Planner.

Frequently Asked Questions

Is Dubai gratuity enough to retire in India?

No. Under Article 51 of the UAE Labour Law, gratuity is capped at two years' basic salary. For someone earning AED 20,000 basic monthly, the maximum is approximately ₹1.1 crore. Most comfortable urban retirements in India require ₹3–8 crore or more.

Can Dubai-based NRIs invest in Indian mutual funds?

Yes. UAE-based NRIs face no FATCA restrictions and can invest with most major AMCs via NRE or NRO accounts. NRE-funded investments are fully repatriable. The India–UAE DTAA reduces double taxation exposure.

What is the minimum SIP amount for an NRI mutual fund investment?

SIPs can start from ₹500 per month at most fund houses. Use the FinAtoZ retirement calculator to work backwards from your inflation-adjusted corpus target to the monthly SIP amount required at your current age.

Book a Consultation

FinAtoZ's Certified Financial Planners work with clients to build personalised, goal-based retirement plans for India. SEBI-registered (INA200006628). Fiduciary. Fee-based.

Book an introductory call or call +91-98800 83712.

Get Expert Financial Advice

Book an introductory call with our Certified Financial Planner to explore how we can help you achieve your financial goals.

About the author

Ashish Vryse